What is Financial Literacy?

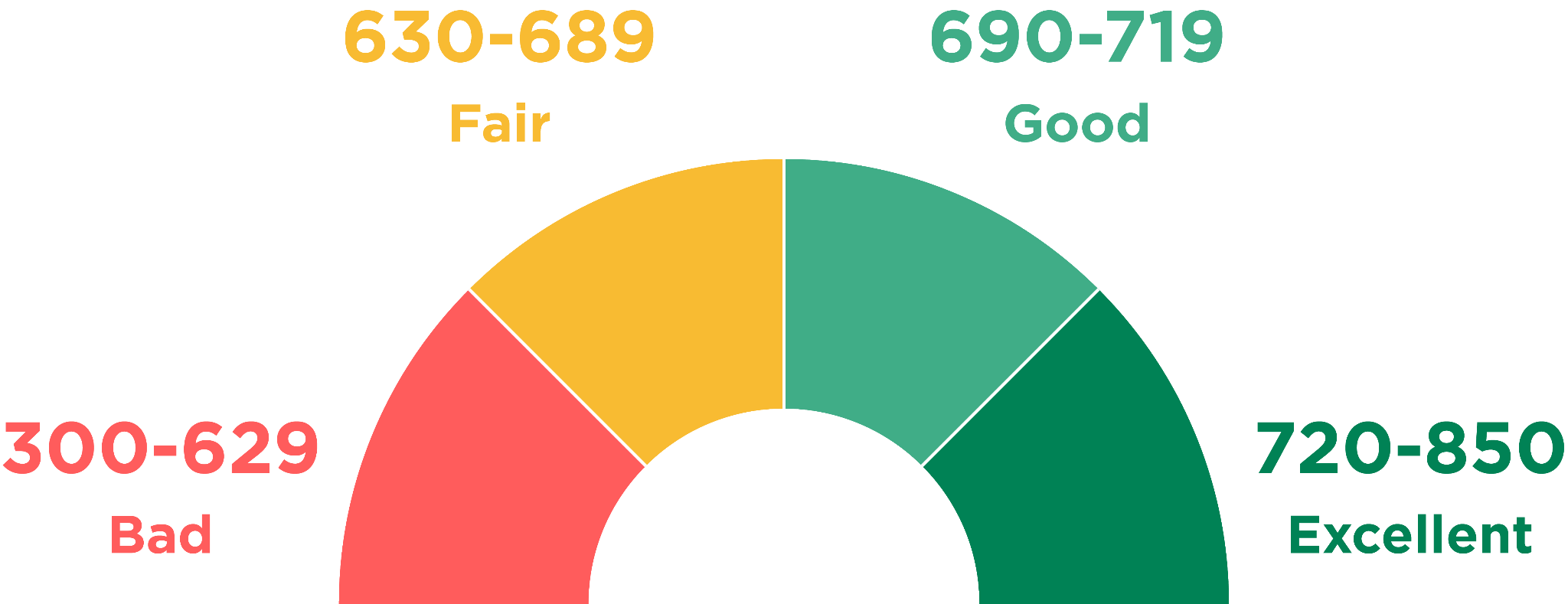

Financial Literacy is the study of making financially smart and responsible decisions. Being financially literate means knowing how to handle and invest your money using different methods. It also entails the areas of debt, learning how to avoid it, and credit, learning how to get and maintain a good credit score, and savings. As said in the article, Money Matters, by Nicole Kruse, financial literacy should be taught to children at an early age, and this can be achieved by incorporating it into the curriculum. Students learning about finances has proven to be very rewarding. Many students graduate high school and don’t have any idea how to live their adult life. If they were learning about finances earlier, they wouldn’t be clueless on how to manage their money. Your credit score is the biggest influence on your finances, so it is important that you maintain a good score. This three digit score determines if you are eligible to buy a house or a car, or borrow a loan. There is no easy or fast way to fix your credit score. Fixing your score takes a lot of patience and time. To improve your credit score, you should pay your bills on time, reduce your debt as much as you can, get credit counselling, check your credit report for errors, and pay off your credit card bills. Using credit cards to pay off debt is not advised because that would be transferring your debt from one place to another. Your savings could be used to pay off debt, but that would mean that you would have no safety net if an unexpected event were to happen. It is not recommended, but if you really need to, that is another way to reduce debt and increase your credit. Savings is an important aspect of financial literacy. There are different ways to save money, two of the most common ones are the ‘piggy bank' method and opening a savings account, which is an account that you open and continuously fund to save money. The ‘piggy bank’ method is probably the most well-known method as it simply consists of putting away a certain amount of money weekly or monthly, and keeping it in a safe place or a piggy bank. The downside of using this method is if your money gets stolen or lost, there will be no way to recover it. Another downside would be not knowing the exact amount of money that is in the piggy bank. Using an actual savings account will give you a more accurate way of checking your balance. An advantage of a savings account is that it is insured by the Federal Deposit Insurance Corporation (FDIC), unlike in the piggy bank method. The act of saving, whether it is just storing money in a piggy bank or using an actual savings account, is recommended because an unexpected event can occur at any time and having money saved can save you from debt in the future. Debt is what you owe, whether it’s an overdue payment or money you borrowed. Managing debt can help your credit score, which in turn could improve the way you live your life. Some ways to stay out of debt include maintaining a good credit score, making and sticking to a list, and not going over budget. If you are already in debt, cutting your spending costs, stop buying impulsively, creating a budget and try to spend within that range, lowering your interest rates, and finding a way to make more money, can help you maintain that debt and slowly reduce it. All these topics are under the financial literacy umbrella and should be taught to all students and not just the ones taking a business major.

Comments

Post a Comment